This article is the first installment in a four part series that talks about the ongoing digital disruption across financial services. This first post sets the stage for the entire market. Subsequent posts will cover each of the mini worlds – Capital Markets, Retail & Consumer Banking & Wealth Management – that comprise the banking industry. Each post will cover the evolving landscape in the given sector and the impact of digitization. We also cover the general business direction in the context of disruptive technology innovation.

The Financial Services Industry is in the midst of a perfect storm. For an industry thats always enjoyed relatively high barriers to entry & safe incumbency, a wave of Fintechs and agile competitors are upending business dynamics across many Banking domains. It is also interesting that while incumbent firms continue to billions of dollars in technology projects to maintain legacy platforms as well as create lateral innovation – the Fintechs are capturing market share using a mix of innovative technology, , as well as creating new products & services – all aimed at disintermediating & disrupting existing value chains via Digital Transformation.

Thus digital disruption has arrived late in financial services as compared to sectors like Retail & Healthcare. In Retail for instance, Amazon.com has caused tectonic shifts for years causing existing brick and mortar players to build out substantial online storefronts which are integrated into backoffice operations and across their supply chains

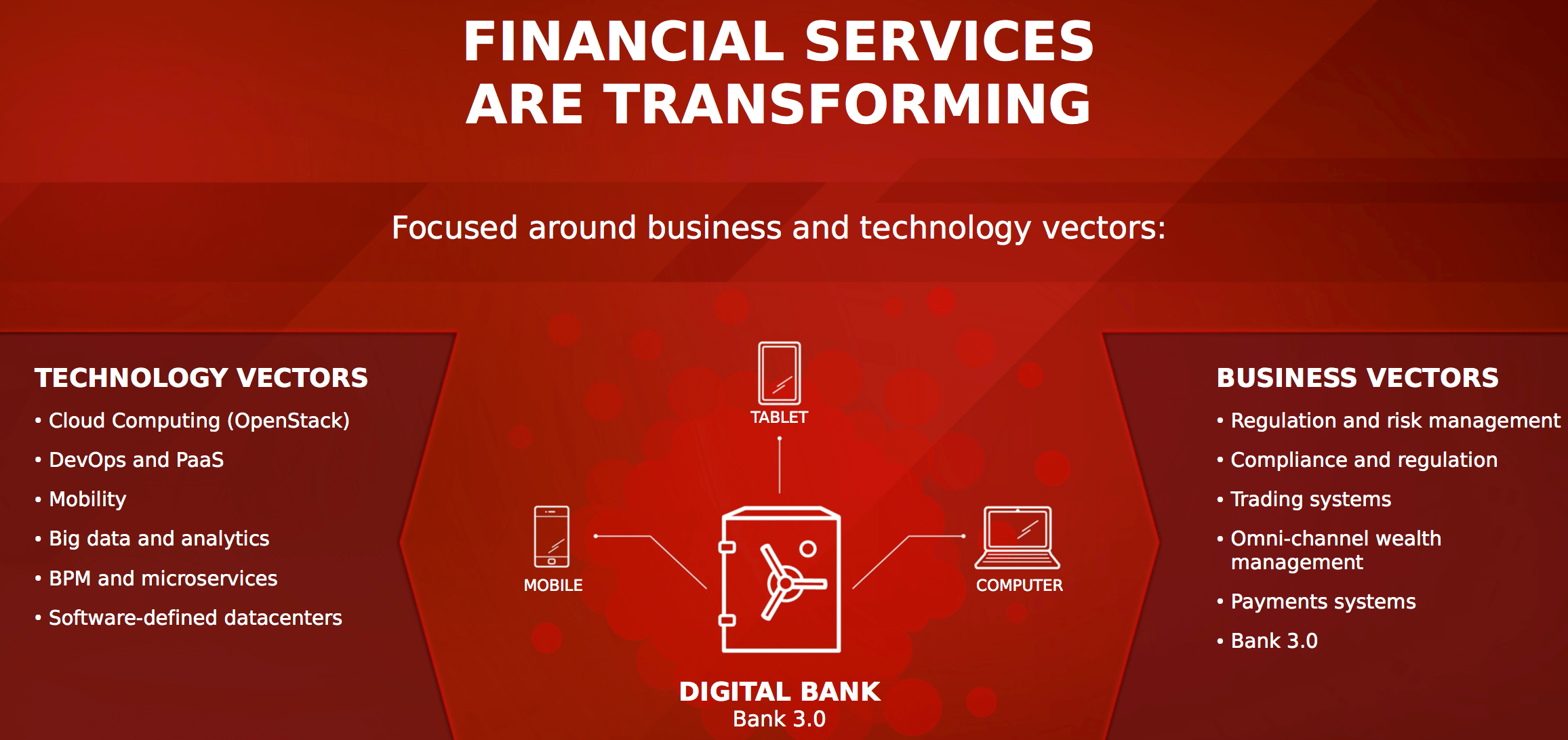

So what are the major technology prongs driving this transformation and how does such an approach boil down in terms of technology principles? And pray, what are the technology ingredients that make up a successful Digital Strategy or more importantly how do all the principles of webscale apply at a large organization? I would wager that there are five or six major factors, chief among them – an intelligent approach to leveraging data (ingesting, mining & linking microfeeds to existing data – thus a deep analytical approach based on predictive analytics and machine learning), an agile infrastructure based on cloud computing principles, a microservice based approach to building out software architectures, mobile platforms that accelerate customers abilities to Bank Anywhere, an increased focus on automation both from a business process to software system delivery and finally a culture that encourages risk taking & a “fail fast” approach.

Thus, the six trends are –

1. Big Data,

2.Cloud Computing,

3.Mobile Computing & Platforms,

4.Social Media,

5.DevOps and Microservices

6.Analytics

Digital Banking is the age of the hyper-connected consumer. Customers are expecting to be able to Bank from anywhere, be it a mobile device or use internet banking from their personal computer. The business areas shown in the above picture are a mix of both legacy capabilities (Risk, Fraud and Compliance) to the new value added areas (Mobile Banking, Payments, Omni-channel Wealth Management etc).

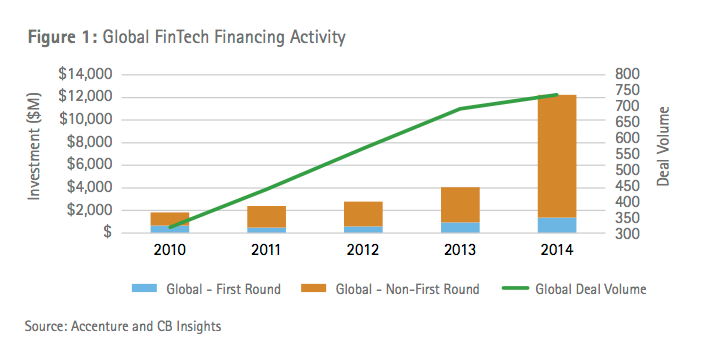

Accenture reports that global investment in Fintech ventures tripled to $12.21 billion in 2014. This clearly signifying that the digital revolution has well and truly arrived in the financial services sector.

What are some of the exciting new business models that the new entrants in Fintech are pioneering at the expense of the traditional Bank ?

- Offering targeted banking services to technology savvy customers at a fraction of the cost e.g. Mint.com in retirement planning in the USA

- Lowering cost of access to discrete financial services for business customers in areas like foreign exchange transactions & payments e.g. Currency Cloud

- Differentiating services like peer to peer lending among small businesses and individuals e.g. Lending Club

- Providing convenience through use of handheld devices like iPhones .e.g. Square Payments

Large Banks, which have built up massive economies of scale over the years, do hold a large first mover advantage. This is due to a range of established services across their large (and loyal) customer bases, rich troves of data that pertain to customer transactions & demographic information. However, it is not enough to just possess the data. They must be able to drive change through legacy thinking and infrastructures.

So what do Banking CXOs need to do to drive an effective program of Digital Transformation?

- Change employee mindset and culture that are largely set on ‘business as usual’ to a mindset of unafraid experimentation across the business areas shown on the right side of the above pictorial

- Create the roles of Digital and Technology entrepreneurs as change agents across these complex technology areas. These leaders should help seed digital thinking into these lines of business

- Drive culture to adapt to new ways of doing business with a population going increasingly digital by offer multiple channels and avenues

- Offer data driven capabilities that can detect customer preferences on the fly, match them with existing history and provide value added services. Services that not only provide a better experience but also help in building a longer term customer relationship

- Help the business & IT rapidly develop, prototype, test new business capabilities

To their credit, the large Banks are not sitting still. Bank of America, as one example has been in the news as bringing in 60% of all it’s sales from Digital Channels from their last quarter – Q2 of 2015.

Bank Of America might want to change its name to Digital Bank of America.

The Charlotte, N.C., megabank is more digital bank than conventional financial institution today. That’s because 60% of the bank’s “sales” are “all digital now,” Brian T. Moynihan, Chairman and CEO of Bank of America, told investors yesterday.

Moynihan also disclosed that about 6% of the bank’s digital “sales” – it is difficult to identify exactly what he means by “sales,” unfortunately – are via mobile device, “and that’s growing at 300%,” he said.

Moynihan’s disclosures yesterday were the most publicly detailed on digital banking at a major bank to date.

Ref – http://bankinnovation.net/2015/07/share-of-digital-sales-at-bank-of-america-hits-60/

The definition of Digital is somewhat nebulous, I would like to define the key areas where it’s impact and capabilities will need to be felt for this gradual transformation to occur.

A true Digital Bank needs to –

- Offer a seamless customer experience much like the one provided by the likes of Facebook & Amazon i.e highly interactive & intelligent applications that can detect a single customer’s journey across multiple channels

- offer data driven interactive services and products that can detect customer preferences on the fly, match them with existing history and provide value added services. Services that not only provide a better experience but also foster a longer term customer relationship

- to be able to help the business prototype, test, refine and rapidly develop new business capabilities

- Above all, treat Digital as a Constant Capability and not as an ‘off the shelf’ product or a one off way of doing things

Though some of the above facts & figures may seem startling, it’s how individual banks put both data and technology to work across their internal value chain that will define their standing in the rapidly growing data economy.