- Full service online Robo-advisor that is a 100% automated without any human element

- Hybrid Robo-advisor model being pioneered by firms like Vanguard & Charles Schwab

- Pure online advisor that is primarily human in nature

What do Robo-advisors typically do?

The Robo-advisor can be optionally augmented & supervised by a human adviser. At the moment, owing to the popularity of Robo-advisors among the younger high networth investors (HNWI), a range of established players like Vanguard, Charles Schwab as well as a number of FinTech start-ups have developed these automated online investment tools or have acquired FinTech’s in this space.e.g Blackrock. The Robo-advisor is typically offered as a free service (below a certain minumum) and typically invests in low cost ETFs. built using digital techniques – such as data science & Big Data.

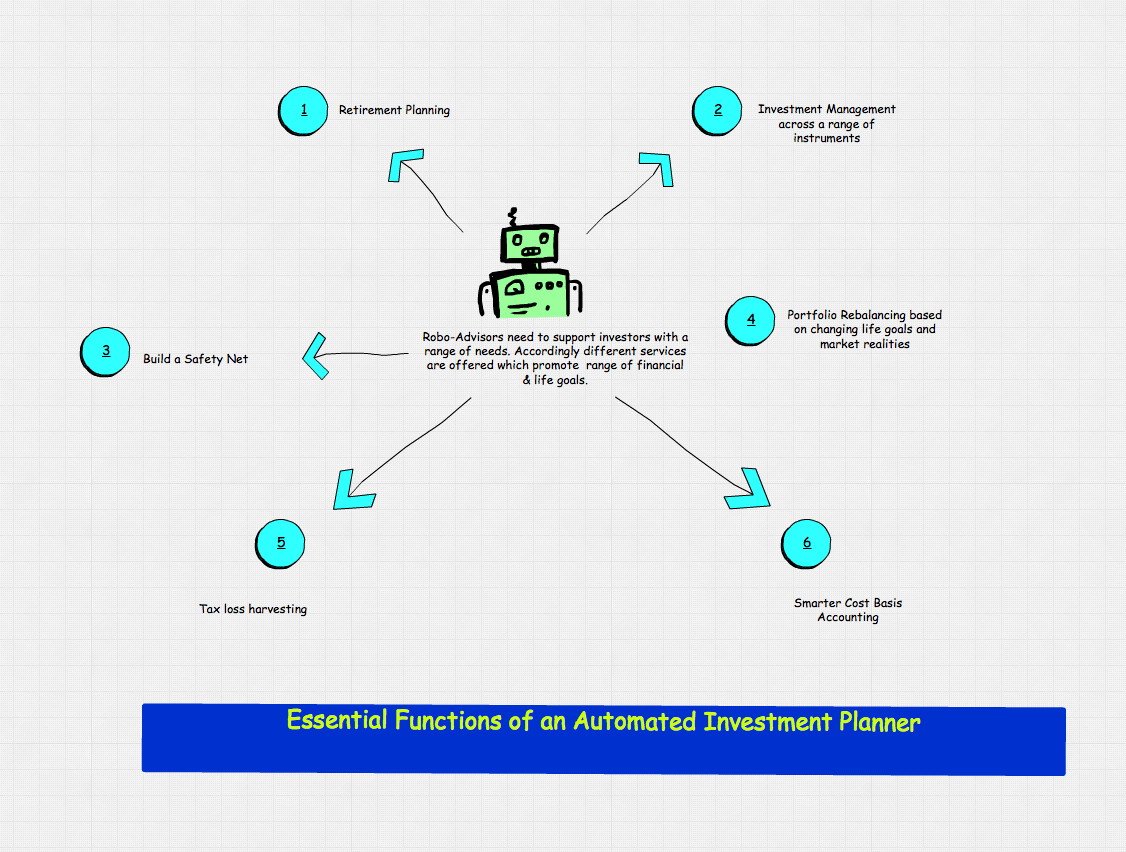

Illustration: Essential functions of a Robo-advisor

The major business areas & client offerings in the Wealth & Asset Management space have been covered in the first post in this series at http://www.vamsitalkstech.com/?p=2329

Automated advisors only cover a subset of all of the above at the moment. The major usecases are as below –

- Determine individual Client profiles & preferences—e.g. For a given client profile- determine financial goals, expectations of investment return, diversification etc

- Identify appropriate financial products that can be offered either as pre-packaged portfolios or custom investments based on the client profile identified in the first step

- Establish correct Investment Mix for the client’s profile – these can included but are not ,limited to equities, bonds, ETFs & other securities in the firm’s portfolios . For instance, placing tax-inefficient assets in retirement accounts like IRA’s as well as tax efficient municipal bonds in taxable accounts etc.

- Using a algorithmic approach, choose the appropriate securities for each client account

- Continuously monitor the portfolio & transactions within it to tune performance , lower transaction costs, tax impacts etc based on how the markets are doing. Also ensure that a client’s preferences are being incorporated so that appropriate diversification and risk mitigation is being performed

- Provide value added services like Tax loss harvesting to ensure that the client is taking tax benefits into account as they rebalance portfolios or accrue dividends.

- Finally ,ensure the best user experience by handling a whole range of financial services – trading, account administration, loans,bill pay, cash transfers, tax reporting, statements in one intuitive user interface.

Illustration: Betterment user interface. Source – Joe Jansen

To illustrate these concepts in action, leaders like Wealthfront & Betterment are increasingly adding features where highly relevant, data-driven advice is being provided based on existing data as well as aggregated data from other providers. Wealthfront now provides recommendations on diversification, taxes and fees that are personalized not only to the specific investments in client’s account, but also tailored to their specific financial profile and risk tolerance. For instance, is enough cash being set aside in the emergency fund ? Is a customer holding too much stock in your employer? [1]

The final post will look at a technology & architectural approach to building out a Robo-advisor. We will also discuss best practices from a WM & industry standpoint in the context of Robo-advisors.

References:

- Wealthfront Blog – “Introducing the new Dashboard”

3 comments

Good thoughts here on robo!

Super post this!

Such an hot topic in the in the fintech market and you already come up with a blue print!

This one is good one for weekend read.

Thank you Sankalp! Appreciate your readership and constant support.