“Banking as a service has long sat at the heart of our economy. In our digitally enabled world, the need to seamlessly and efficiently connect different economic agents who are buying and selling goods and services, is critical. The Open Banking Standard is a framework for making banking data work better: for customers; for businesses and; for the economy as a whole.” – OBWG (Open Bank Working Group) co-chair and Barclays executive Matt Hammerstein

Introducing Open Banking Standards…

On a global basis, both the Financial Services and the Insurance industry are facing an unprecedented amount of change driven by factors like changing client preferences and the emergence of new technology—the Internet, mobility, social media, etc. These changes are immensely profound, especially with the arrival of the “FinTechs”—technology-driven applications that are upending long-standing business models across all sectors from retail banking to wealth management & capital markets. Complement this with members of a major new segment, Millennials. They are increasingly use mobile devices, demanding more contextual services and expecting a seamless unified banking experience—something akin to what they experience on web properties like Facebook, Amazon, Uber, Google or Yahoo, etc. These web scale startups are doing so by expanding their wallet share of client revenues by offering contextual products tailored to individual client profiles. Their savvy use of segmentation data and predictive analytics enables the delivery of bundles of tailored products across multiple delivery channels (web, mobile, call center banking, point of sale, ATM/kiosk etc.).

Supra national authorities and national government in Europe have taken note of the need for erstwhile protected industries like Banking to stay competitive in this brave new world.

With the passage of the second revision of the ground breaking Directive on Payment Services Directive (PSD-2), the European Parliament has adopted the legal foundation of the creation of a EU-wide single payments area (SEPA)[1]. While the goal of the PSD is to establish a set of modern, digital industry rules for all payment services in the European Union; it has significant ramifications for the financial services industry as it will surely current business models & foster new areas of competition. While the PSD-2 has gotten the lions share of press interest, the UK government has quietly been working on an initiative to create a standard around allowing Banking organizations to share their customer & transactional data with certified third parties via an open API. The outgoing PM David Cameron’s government had in fact outlined these plans in the 2015 national budget.

The EU and the UK governments have recognized that in order for Europe to move into the vision of one Digital Market – the current system of banking calls for change. And they foresee this change will be driven by digital technology. This shakeup will happen via the increased competition that will result as various financial services are unbundled by innovative developers. To that end, by 2019 – all banks should make customer data – their true crown jewels – openly accessible via an open standards based API.

The Open Bank Working Standard Report API…

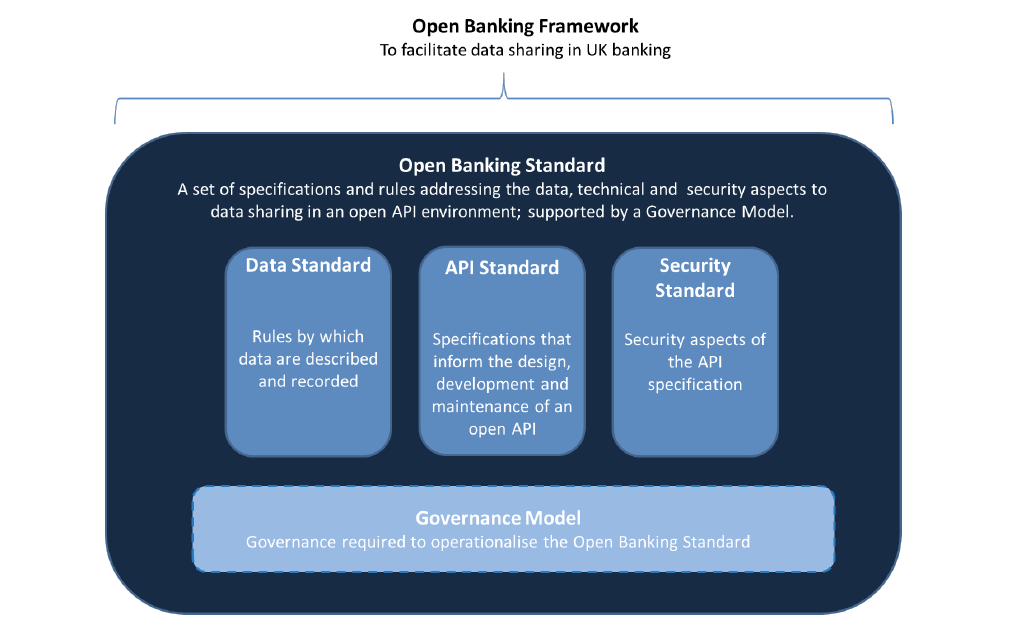

Illustration: Components of the Open Banking Standard (ref – OBWG Working Group)

Under the Open Banking Standard – expected to be legal reality over the next 2-3 years, any banking customer or authorized 3rd party provider can leverage APIs to gain access to their data and transactions across a whole range of areas ranging from Retail Banking to Business Banking to Commercial Banking.

Open Standards can actually help banks by helping them source data from external providers. For instance, the Customer Journey problem has been an age old issue in banking which has gotten exponentially more complicated over the last five years as the staggering rise of mobile technology and the Internet of Things (IoT) have vastly increased the number of enterprise touch points that customers are exposed to in terms of being able to discover & purchase new products/services. In an OmniChannel world, an increasing number of transactions are being conducted online. In verticals like Retail and Banking, the number of online transactions approaches an average of 40%. Adding to the problem, more and more consumers are posting product reviews and feedback online. Banks thus need to react in realtime to piece together the source of consumer dissatisfaction. Open Standards will help increase the ability of banks to pull in data from external sources to enrich their limited view of customers.

The Implications of Open Bank Standard…

The five implications of Open Bank Project –

- Banks will be focused on building platforms that can drive ecosystems of applications around them. Banks have thus far been largely focused on delivering commodity financial services using well understood distribution strategies. Most global banks have armies of software developers but their productivity around delivering innovation has been close to zero. Open APIs will primarily force more thinking around how banking products are delivered to the end consumer. The standards for this initiative are primarily open source in origin, though they’re widely accepted across the globe – REST,OAuth etc.

- However it is not a zero sum game, Banks can themselves benefit by building business models around monetizing their data assets as their distribution channels will go global & costs will change around Open Bank. To that end existing Digital efforts should be brought in line with Open Bank Standard The best retail banks will not only seek to learn from, but sometimes partner with, emerging fintech players to integrate new digital solutions and deliver exceptional customer experience. To cooperate and take advantage of fintechs, banks will require new partnering capabilities. To heighten their understanding of customers’ needs and to deliver products and services that customers truly value, banks will need new capabilities in data management and analytics. Using Open Bank APIs, developers across the world can create applications that offer new services (in conjunction with retailers, for example), aggregate financial information or even help in financial planning. Banks will have interesting choices to make between acting as Data Producer or Consumer or Aggregator or even a Distributor based on specific business situations.

- Regulators will also benefit substantially by using Partner APIs to both access real time reports & share data across a range of areas. The lack of realtime data access across a range of risk, compliance and cyber areas has been a long standing problem that can be solved by an open standards based API framework [2]. E.g. Market/Credit/Basel Risk Based Reporting, AML watch list data and Trade Surveillance etc.

- Data Architectures are key to Open Bank Standard – Currently most industry players are woeful at putting together a comprehensive Single View of their Customers (SVC). Due to operational data silos, each department possess a siloe-d & limited view of the customer across multiple channels. These views are typically inconsistent, lack synchronization with other departments & miss a high amount of potential cross-sell and up-sell opportunities. Data lakes and realtime data processing techniques will be critical to meeting this immense regulatory requirement.

- Despite the promise, large gaps still remain in the Open Bank Project. Critical areas like project governance, Service Level Agreements (SLA) for API users in terms of uptime, quality of service are still left unaddressed.

Open Banking Standard will spur immense changes..

Prior to the Open Banking Standard, Banks recognize the need to move to a predominantly online model by providing consumers with highly interactive, engaging and contextual experiences that span multiple channels—branch banking, eBanking, POS, ATM, etc. Business goals are engagement & increasing profitability per customer for both micro and macro customer populations with the ultimate goal of increasing customer lifetime value (CLV). The Open Banking Standard brings technology approaches to the fore in terms of calling it out as a strategic differentiator. Banks need to move to a fresh business, data and process approach as a way of staying competitive and relevant. Done right, Open Bank Standards will help the leaders cement their market position.

REFERENCES…

[1] The Open Banking Standard –

https://theodi.org/open-banking-standard

[2]Big Data – Banking’s New Weapon Against Financial Crime – http://www.vamsitalkstech.com/?p=806