The neighborhood bank branch is on the way out and is being slowly phased out as the primary mode of customer interaction for Banks. Banks across the globe have increased their technology investments in strategic areas such as Analytics, Data & Mobile. The Bank of the future increasingly resembles a technology company.

“I have no doubt that the financial industry will face a series of Uber moments,” – Antony Jenkins (then CEO) of Barclays Bank, 2015

The Washington Post proclaimed in an article [1] this week that bank branch on the corner of Main Street may not be there much longer.

Technology is transforming Banking thus leading to dramatic changes in the landscape of customer interactions. We live in the age of the Digital Consumer – Banking in the age of the hyper-connected consumer. As millenials join the labor force, they are expecting to be able to Bank from anywhere, be it a mobile device or use internet banking from their personal computer.

As former Barclays CEO Antony Jenkins described it in a speech given last fall, the global banking industry, which is under severe pressure from customer demands for increased automation and contextual services, will slash employment and branches by 20 percent to 50 percent over the next decade.[2]

“I have no doubt that the financial industry will face a series of Uber moments,” he said in the late-November speech in London, referring to the way that Uber and other ride-hailing companies have rapidly unsettled the taxi industry.[2]

Banking must trend Digital to respond to changing client needs –

The Financial Services and the Insurance industry are facing an unprecedented amount of change driven by factors like changing client preferences and the emergence of new technology—the Internet, mobility, social media, etc. These changes are immensely profound, especially with the arrival of “FinTech”—technology-driven applications that are upending long-standing business models across all sectors from retail banking to wealth management & capital markets. Further, members of a major new segment, Millennials, increasingly use mobile devices, demand more contextual services and expect a seamless unified banking experience—something akin to what they experience on web properties like Facebook, Amazon, Uber, Google or Yahoo, etc.

The definition of Digital is somewhat nebulous, I would like to define the key areas where it’s impact and capabilities will need to be felt for this gradual transformation to occur.

A true Digital Bank needs to –

- Offer a seamless customer experience much like the one provided by the likes of Facebook & Amazon i.e highly interactive & intelligent applications that can detect a single customer’s journey across multiple channels

- offer data driven interactive services and products that can detect customer preferences on the fly, match them with existing history and provide value added services. Services that not only provide a better experience but also foster a longer term customer relationship

- to be able to help the business prototype, test, refine and rapidly develop new business capabilities

- Above all, treat Digital as a Constant Capability and not as an ‘off the shelf’ product or a one off way of doing things

Though some of the above facts & figures may seem startling, it’s how individual banks put both data and technology to work across their internal value chain that will define their standing in the rapidly growing data economy.

Enter the FinTechs –

FinTechs (or new Age financial industry startups) offer enhanced customer experiences built on product innovation and agile business models. They do so by expanding their wallet share of client revenues by offering contextual products tailored to individual client profiles. Their savvy use of segmentation data and predictive analytics enables the delivery of bundles of tailored products across multiple delivery channels (web, mobile, Point Of Sale, Internet, etc.). Like banks, these technologies support multiple modes of payments at scale, but they aren’t bound by the same regulatory and compliance regulations as are banks, who operate under a mandate that they must demonstrate that they understand their risk profiles. Compliance is an even stronger requirement for banks in areas around KYC (Know Your Customer) and AML (Anti Money Laundering) where there is a need to profile customers—both individual & corporate—to decipher if any of their transaction patterns indicate money laundering, etc.

Banking produces the most data of any industry—rich troves of data that pertain to customer transactions, payments, wire transfers and demographic information. However, it is not enough for financial service IT departments to just possess the data. They must be able to drive change through legacy thinking and infrastructures as the industry changes—both from a data product as well as from a risk & compliance standpoint.

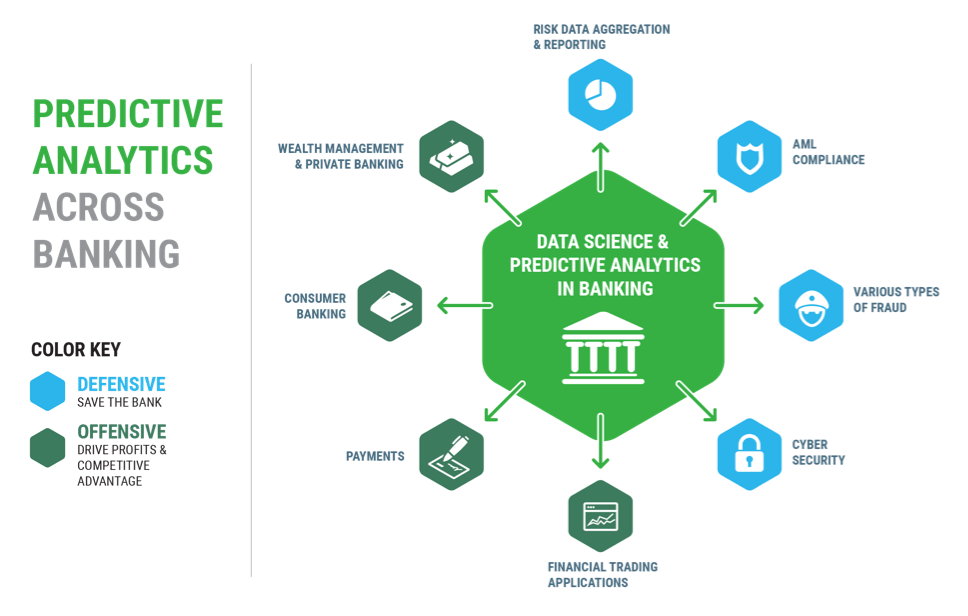

The business areas shown in the below illustration are a mix of both legacy capabilities (Risk, Fraud and Compliance) to the new value added areas (Mobile Banking, Payments, Omni-channel Wealth Management etc).

Illustration – Predictive Analytics and Big Data are upending business models in Banking across multiple vectors of disruption

Business Challenges facing banks today

Banks and other players across the financial spectrum face challenges across three distinct areas. First and foremost they need to play defense with a myriad of regulatory and compliance legislation across defensive areas of the business such as risk data aggregation and measurement and financial compliance and fraud detection. On the other hand, there is a distinct need to vastly improve customer satisfaction and stickiness by implementing predictive analytics capabilities and generating better insights across the customer journey thus driving a truly immersive digital experience. Finally, banks need to leverage their mountains of data assets to create new business models and go-to-market strategies. They need to do this by monetizing multiple data sources—both data-in-motion and data-at-rest—for actionable intelligence.

Data is the single most important driver of bank transformation, impacting financial product selection, promotion targeting, next best action and ultimately, the entire consumer experience. Today, the volume of this data is growing exponentially as consumers increasingly share opinions and interact with an array of smart phones, connected devices, sensors and beacons emitting signals during their customer journey.

Data Challenges –

Business and technology leaders are struggling to keep pace with a massive glut of data from digitization, the internet of things, machine learning, and cybersecurity for starters. A data lake—which combines data assets, technology and analytics to create enterprise value at a massive scale—can help businesses gain control over their data.

Fortunately, Big Data driven predictive analytics is here to help. The Hadoop platform and ecosystem of technologies have matured considerably and have evolved to supporting business critical banking applications. The emergence of cloud platforms is helping in this regard.

Positively impacting the banking experience requires data

Whether at the retail bank or at corporate headquarters, there are a number of ways to leverage technology in order to enable a successful consumer experience across all banking sectors:

Retail & Consumer Banking

Banks need to move to a predominantly online model, providing consumers with highly interactive, engaging and contextual experiences that span multiple channels—branch banking, eBanking, POS, ATM, etc. Further goals are increased profitability per customer for both micro and macro customer populations with the ultimate goal of increasing customer lifetime value (CLV).

Capital Markets

Capital markets firms must create new business models and offer superior client relationships based on their data assets. Those that leverage and monetize their data assets will enjoy superior returns and raise the bar for the rest of the industry. It is critical for capital market firms to better understand their clients (be they institutional or otherwise) from a 360-degree perspective so they can be marketed to as a single entity across different channels—a key to optimizing profits with cross selling in an increasingly competitive landscape.

Wealth Managers

The wealth management segment (e.g., private banking, tax planning, estate planning for high net worth individuals) is a potential high growth business for any financial institution. It is the highest touch segment of banking, fostered on long-term and extremely lucrative advisory relationships. It is also the segment most ripe for disruption due to a clear shift in client preferences and expectations for their financial future. Actionable intelligence gathered from real-time transactions and historical data becomes a critical component for product tailoring, personalization and satisfaction.

Corporate Banking

The ability to market complex financial products across a global corporate banking client base is critical to generating profits in this segment. It’s also important to engage in risk-based portfolio optimization to predict which clients are at risk for adverse events like defaults. In addition to being able to track revenue per client and better understand the entities they bank with, it is also critical that corporate banks track AML compliance.

The future of data for Financial Services

Understand the Customer Journey

Across retail banking, wealth management and capital markets, a unified view of the customer journey is at the heart of the bank’s ability to promote the right financial product, recommend a properly aligned portfolio products, keep up with evolving preferences as the customer relationship matures and accurately predict future revenue from a customer. But currently most retail, investment banks and corporate banks lack a comprehensive single view of their customers. Due to operational silos, each department has a limited view of the customer across multiple channels. These views are typically inconsistent, vary quite a bit and result in limited internal collaboration when servicing customer needs. Leveraging the ingestion and predictive capabilities of a Big Data platform, banks can provide a user experience that rivals Facebook, Twitter or Google and provide a full picture of customer across all touch points.

Create Modern data applications

Banks, wealth managers, stock exchanges and investment banks are companies run on data—data on deposits, payments, balances, investments, interactions and third-party data quantifying risk of theft or fraud. Modern data applications for banking data scientists may be built internally or purchased “off the shelf” from third parties. These new applications are powerful and fast enough to detect previously invisible patterns in massive volumes of real-time data. They also enable banks to proactively identify risks with models based on petabytes of historical data. These data science apps comb through the “haystacks” of data to identify subtle “needles” of fraud or risk not easy to find with manual inspection.

These modern data applications make Big Data and data science ubiquitous. Rather than back-shelf tools for the occasional suspicious transaction or period of market volatility, these applications can help financial firms incorporate data into every decision they make. They can automate data mining and predictive modeling for daily use, weaving advanced statistical analysis, machine learning, and artificial intelligence into the bank’s day-to-day operations.

Conclusion – Banks need to drive Product Creation using the Latest Technology –

A strategic approach to industrializing analytics in a Banking organization can add massive value and competitive differentiation in five distinct categories –

- Exponentially improve existing business processes. e.. Risk data aggregation and measurement, financial compliance, fraud detection

- Help create new business models and go to market strategies – by monetizing multiple data sources – both internal and external

- Vastly improve customer satisfaction by generating better insights across the customer journey

- Increase security while expanding access to relevant data throughout the enterprise to knowledge workers

- Help drive end to end digitization

If you really think about it – all that banks do is manipulate and deal in data. If that is not primed for a Über type of revolution I do not know what is.

References

[1] https://www.washingtonpost.com/news/wonk/wp/2016/04/19/say-goodbye-to-your-neighborhood-bank-branch/

[2] http://www.theguardian.com/business/2015/nov/25/banking-facing-uber-moment-says-former-barclays-boss